Life insurance

Life assurance pays out a lump sum when you pass away, helping your loved ones cover things like living costs, debts, or funeral expenses. It’s a way to give them financial support when they need it most.

Get in touch

If you have a quick question, fill-in this form:

Looking to discuss a mortgage?

If you would like to discuss your mortgage requirements with an advisor, please click here to provide more details and speed-up the process.

If you were no longer here tomorrow, who would your family call first? One of those calls would likely be to your mortgage provider, and without life assurance in place, they could be met with legal steps, financial pressure, or even the risk of losing the family home. Life assurance is designed to prevent that. There are two types of cover: Decreasing Life Assurance & Term Life Assurance.

In many cases, both types of policy include a terminal illness benefit, meaning if you’re diagnosed with a condition expected to result in death within 12 months, a lump sum is paid out early. Importantly, the payout from life insurance doesn’t have to go towards the mortgage - it can be used however your loved ones need it most. Whether it’s covering bills, childcare, or giving them breathing space during a difficult time, it’s there to support your dependents when they need it most.

PROTECT YOUR MORTGAGE WITH MORTGAGE LIGHT

What are the different types of cover?

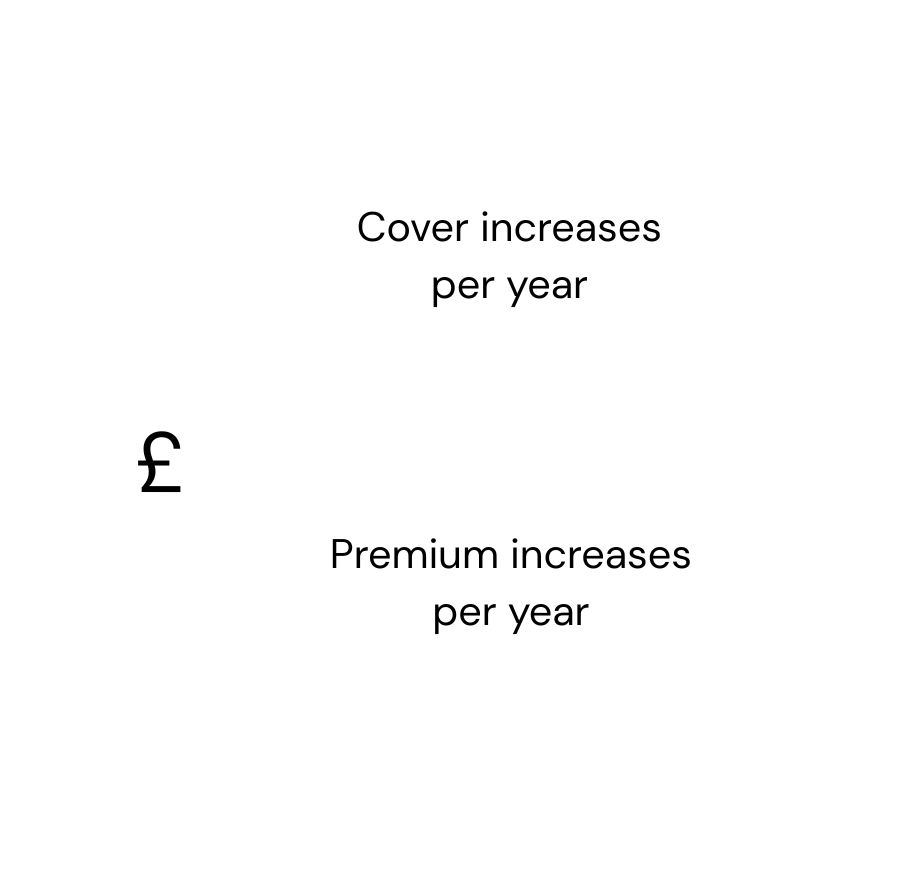

Term life assurance

Helps protect your cover against the effects of inflation, giving added protection for you and your loved ones. Term Life Assurance is the opposite of Decreasing Life Assurance in that the amount of cover remains the same throughout the term of the policy and does not reduce.

This type of Life Assurance is suitable for those people with interest only mortgages, and also those wanting to leave a sum of money behind to ensure their family's standard of living.

- Cover remains the same throughout the term of the policy

- Premiums calculated when you take out the policy, and stay the same for the duration of the policy term

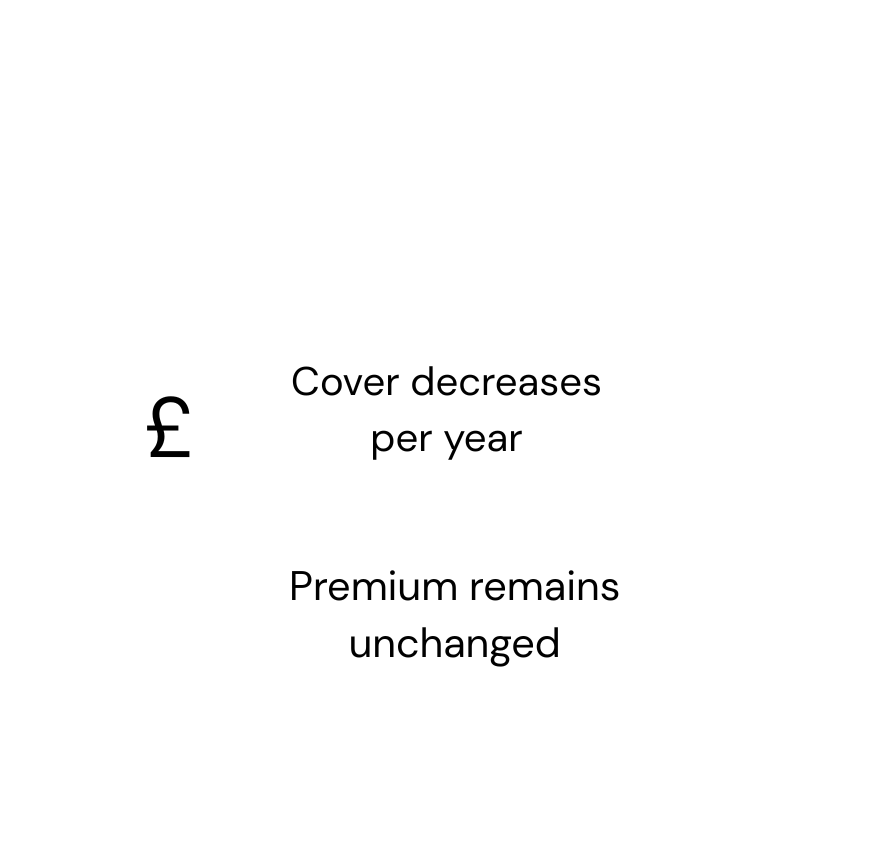

Decreasing cover

Helps to pay off debt that's reducing over time, like a mortgage. Decreasing Life Assurance is most suitable for mortgages which are Capital Repayment, this is because the level of cover is designed to reduce as your mortgage reduces over the years. The reduction ensures that there is always enough in the 'pot' to pay off the mortgage if the worst happens but there will be very little surplus remaining.

It’s typically more affordable than other types of life insurance, making it a popular choice for homeowners.

- Cover amount decreases each month broadly in line with a repayment loan using a fixed interest rate

- Premiums calculated when you take out the policy, and stay the same for the duration of the policy term

PROTECT YOU AND YOUR FAMILY's FINANCes.

Added value benefits you might not expect

Many modern income protection policies now include a range of additional benefits, some standard, others optional - offering broader family support. These may include:

Parent & child cover

Lump sum payouts if your child is diagnosed with a serious illness.

Fracture cover

Financial support for specific bone injuries, often paid alongside your monthly benefit.

Death benefit

A fixed payment to your family if you die during the policy term.

Payment breaks

Some policies pause premiums for up to 6 months in the event of involuntary unemployment.

Mental health & wellbeing

private GP access or physiotherapy as part of the policy.

Pregnancy cover

Financial support or lump sums for specific pregnancy complications.

Global treatment

Cover for specialist overseas treatment if it isn’t available locally.

💡 Working with the leading lenders in the whole of market...

SEE WHAT OUR CLIENTS HAVE TO SAY...

Testimonials

HOMEOWNERSHIP FOR EVERYONE.

10 ways first time buyers are getting on the property ladder

As a first-time buyer, there are a number of mortgage products designed to help make homeownership more accessible - particularly if you’re struggling to build up a large deposit.

Low deposit mortgages

Where some lenders will accept deposits as low as 5%, depending on your credit profile and income.

Higher income multiples

Available to applicants with strong rental histories, a high salary, or professional qualifications, often more accessible when you have a larger deposit

Cashback mortgages

A fixed sum back upon completion to help with initial costs - normally linked to new build homes.

Shared ownership

Where you buy a share of a property and pay rent on the remainder – with the option to purchase more shares over time.

Builder or developer incentives

Often offered on new-builds to reduce your upfront costs - there are often ways to work directly with the developer to tailor the deal and explore additional mortgage options.

Joint borrower, sole proprietor mortgages

Sometimes called “income booster” - allowing a parent or family member to support your income without being named on the property

Zero deposit (100%) mortgages

Available in specific circumstances – such as where you've been renting for a period of time and can show a consistent payment record. These are subject to stricter eligibility criteria and affordability checks.

Looking to get more information on your first mortgage?

PROTECT YOURSELF WITH MORTGAGE LIGHT.

Our team are here to help.

We make this easy for you. Simply contact us to arrange to come in and discuss your needs. If you’re pushed for time, call one of our expert advisers and we will be able to go through your options in a quick chat over the phone.